인플레이션이 치솟으면서 2분기 수익 시즌을 미리 보고 있습니다.

연준의 긴축에 직면하여 수익 추정치가 내려가는 것은 타당합니다. 그 이유는 높은 이자율로 인해 경제 성장이 더뎌지고, 결과적으로 수익 증가가 완만해지는 ‘제2의 파생’ 효과입니다.

시장에는 연준이 경제를 경기 침체로 몰아넣지 않고 인플레이션 문제를 극복하는 것을 볼 수 없는 일부 사람들이 있습니다. 이러한 관점의 다양성은 저명한 비즈니스 리더들의 공개적인 논평과 심지어 수익률 곡선이 다시 역전되는 것처럼 보이는 채권 시장에서 나타납니다.

경제에 대한 침체된 결과는 합의된 관점도 아니고 잭스 경제팀이 현재 예측하고 있는 것도 아니다. 하지만, 모든 사람들이 동의하는 것은 높은 금리의 누적 효과가 경제에 스며들면서 경제가 둔화되기 시작해야 한다는 것입니다.

지난 금요일 예상보다 나은 5월 일자리 보고서가 보여주었듯이, 우리는 아직 거기까지 가지 못했습니다. 그러나 일부 기업들은 채용 동결 또는 해고를 발표하면서 몇 가지 분명한 완화 조짐이 보이기 시작했습니다. 심지어 강력한 5월 일자리 보고서도 임금 상승이 다소 둔화되는 모습을 보였습니다.

아직은 이르지만, 이러한 징후들은 연준의 조치가 바람직한 방향으로 경제를 이끌고 있다는 것을 암시합니다. 즉, 최근 인플레이션 수치(6월 10일자 5월 CPI 보고서)는 중앙은행이 경제 전반의 가격 압력이 완화되기 시작하기 전에 한동안 인플레이션 박자를 유지할 필요가 있음을 보여줍니다.

경제성장의 완화에 따른 ‘제2의 파생효과’로 돌아가기 위해, 우리는 수익 추정치가 다소 낮아지긴 했지만, 상당한 경기 둔화와 일치하는 수준에는 전혀 미치지 못한다는 점에 주목합니다.

예를 들어, S&P 500 지수 기업의 2022년 2분기 수익은 현재 전년 동기 대비 +1.9% 증가하여 수익은 +9.5% 증가할 것으로 예상됩니다.

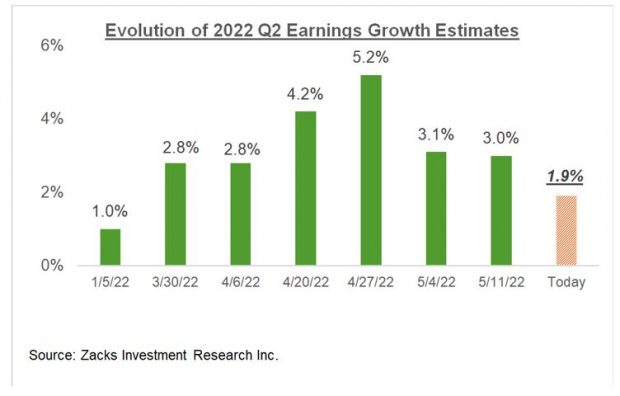

S&P 500 수준에서 총 수정 추세를 살펴보면, 아래 도표에서 볼 수 있듯이, 2022년 시작 이후 지수에 대한 총 2분기 수익 성장 추정치의 진화를 보여주는 많은 움직임이 보이지 않습니다.

img src=”https://staticx-tuner.zacks.com/images/articles/charts/cd/22780.jpg?v=1772477539″>

이미지 출처: Jacks Investment Research입니다.

이 차트는 3월 30일의 2분기 예상 수익 성장률이 2.8%에서 오늘 1.9%로 하락했음을 보여줍니다.

즉, 에너지 부문에 대한 긍정적인 수정이 대부분의 다른 부문의 감소를 상쇄하는 등 섹터 수준에는 많은 교차 전류가 존재합니다.

잭스 에너지 부문의 2022년 2분기 수익 추정치는 4월 초부터 +47.9% 증가했습니다.

에너지 부문만이 2분기 추정치를 긍정적으로 수정한 것은 아닙니다. 다른 5개 부문에서도 추정치가 다양한 규모로 상향 조정되었습니다.

4월 1일 2분기 시작 이후 운송, 기초 자재, 자동차, 건설 및 소비자 필수품 부문의 수익 추정치가 상승했습니다. 이 5개 부문 중 교통 및 기초 자재 부문에서 2분기 실적 전망으로의 업그레이드가 특히 중요합니다.

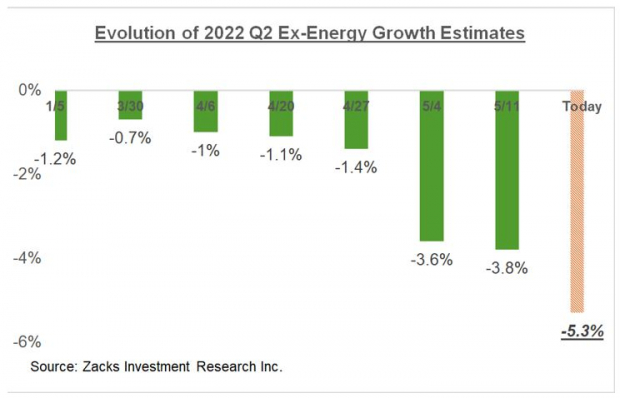

총 2분기 개정판을 살펴보면, 혼합에서 에너지 섹터를 제외한 후 아래와 같이 그림이 바뀝니다.

img src=”https://staticx-tuner.zacks.com/images/articles/charts/8a/22781.jpg?v=680837874″>

이미지 출처: Jacks Investment Research입니다.

연간 기준 개정 시에도 거의 동일한 추세가 나타나고 있습니다. 총 추정치는 연초 이후 안정적이거나 다소 증가했지만 에너지 사용량을 제외하고 감소하기 시작했습니다.

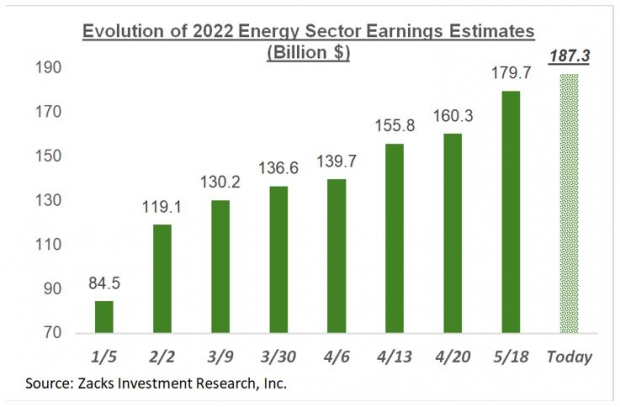

이 부분의 길이를 관리하기 위해 이 차트를 여기서 공유하지는 않겠지만, 연초부터 에너지 부문의 2022년 전체 수익 추정치가 어떻게 되었는지 살펴보는 것이 유용할 것이라고 생각합니다.

img src=”https://staticx-tuner.zacks.com/images/articles/charts/d8/22782.jpg?v=1748904120″>

이미지 출처: Jacks Investment Research입니다.

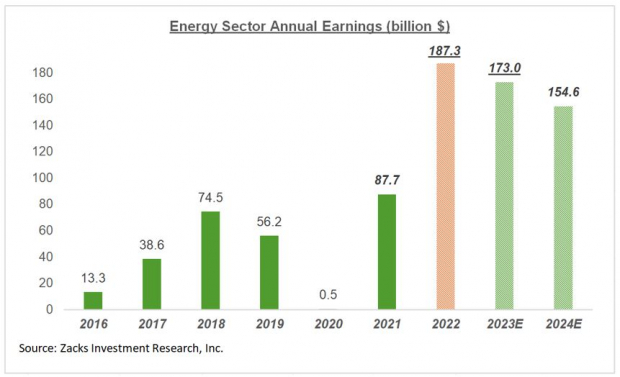

어쨌든, 에너지 부문은 현재 매우 강력한 수익 전망과 함께 좋은 위치에 있습니다. 이 부문의 수익에 대한 비교적 장기적인 관점은 아래에 강조되어 있습니다.

img src=”https://staticx-tuner.zacks.com/images/articles/charts/00/22783.jpg?v=260583020″>

이미지 출처: Jacks Investment Research입니다.

이번 주의 수익 결과입니다.

이번 주 분기 실적을 보고하기 위해 S&P 500 회원 3명이 갑판에 배치되어 있습니다. Kroger KR, Oracle ORCL 및 Adobe ADBE입니다. 이 세 가지 중 Oracle과 Adobe는 5월에 종료되는 각 회계 분기에 대한 결과를 보고할 예정이며, Kroger는 4분기 결과를 보고할 예정입니다.

NAT과 다른 데이터 공급업체가 사용하는 규약은 이번 주 Kroger 결과를 2022년 1분기 집계 결과에 포함시키고, Adobe 및 Oracle 결과는 2022년 2분기 집계 결과에 포함시킵니다.

두 인덱스 멤버인 Costco COST와 AutoZone AZO가 이미 2022년 2분기 집계로 분류한 5분기 회계 결과를 발표했기 때문에 Adobe와 Oracle이 2분기 결과를 보고한 첫 번째 S&P 500 멤버가 아니라는 점에 유의하십시오.

2분기 보고 주기는 대형 은행들이 분기별 실적을 발표하는 7월 중순에 본격적으로 시작될 것입니다. 그러나 우리는 그때까지 거의 24개 지수 회원들로부터 그러한 2분기 결과를 계산해 냈을 것입니다.

현재 수익 배경입니다.

아래 차트는 분기별로 현재 예상(및 실제)을 보여 줍니다.

img src=”https://staticx-tuner.zacks.com/images/articles/charts/8c/22784.jpg?v=1144071505″>

이미지 출처: Jacks Investment Research입니다.

향후 기간에 대한 기대치를 포함하여 전반적인 수익 상황을 자세히 보려면 주간 수익 동향 보고서를 참조하십시오>>>기술 부문의 수익 전망 분석

방금 출시된 br: 잭스는 2022년 상위 10개 종목에 선정되었습니다.

위에서 논의한 투자 아이디어 외에도, 2022년 전체 Top Pick 10에 대해 알고 싶으십니까?

2012년부터 2021년까지 잭스 상위 10개 주식 포트폴리오는 S&P 500의 +348.7%에 비해 +1,001.2%의 놀라운 수익을 얻었습니다. 이제 당사의 연구 책임자는 잭스 등급의 대상이 되는 4,000개의 회사를 샅샅이 뒤졌고 구매 및 보유할 수 있는 가장 좋은 10개의 항공권을 직접 선정했습니다. 기회를 놓치지 마십시오. 기회를 빨리 잡을수록 유리한 고지를 점할 수 있습니다.

지금 주식을 보세요>>

무료 보고서를 가져오려면 클릭하십시오.

크로거 주식회사(KR): 자유 재고 분석 보고서입니다.

Oracle Corporation(ORCL): 무료 재고 분석 보고서입니다.

코스트코 도매법인(COST): 무료 재고 분석 보고서입니다.

Adobe Inc.(ADBE): 무료 재고 분석 보고서입니다.

AutoZone, Inc.(AZO): 무료 재고 분석 보고서입니다.

이 기사 onZacks.com를 읽으려면 여기를 클릭하십시오.

Jacks Investment Research 여기에 표현된 견해와 의견은 저자의 견해와 의견이며 반드시 나스닥, Inc.의 견해를 반영하는 것은 아니다.

It is reasonable for earnings estimates to be coming down in the face of Fed tightening. The reason for that is the ‘second-derivative’ effect, with higher interest rates resulting in slower economic growth which in turn shows up in moderating revenue growth.

There are some in the market that can’t see the Fed getting on top of the inflation problem without pushing the economy into a recession. Variations of this view show up in public comments from prominent business leaders and even the bond market where the yield curve appears again to be heading towards inversion.

A recessionary outcome for the economy is neither the consensus view nor what the Zacks economic team is projecting at present. What everyone agrees on, however, is that the economy should start slowing as the cumulative effect of higher interest rates seep through into the economy.

We are not there yet, as the better-than-expected May jobs report showed last Friday. But we are starting to see some tell-tale signs of moderation, with some companies announcing hiring freezes or even lay-offs. Even the strong May jobs report showed some deceleration in wage gains.

It is still early, but these signs suggest that the Fed’s actions are steering the economy in the desirable direction. That said, the latest inflation reading (May’s CPI report from June 10th) shows that the central bank will need to stay on the inflation-fighting beat for some time before economy-wide pricing pressures will start easing.

To get back to the ‘second-derivative’ effect of moderating economic growth, we note that while earnings estimates have come down a bit, they are nowhere near what would be consistent with a significant economic slowdown.

For example, 2022 Q2 earnings for the S&P 500 index companies are currently expected to increase +1.9% from the year-earlier level on +9.5% higher revenues.

If we look at the revisions trend in the aggregate, at the S&P 500 level, we don’t see a lot of movement, as you can see in the chart below that plots the evolution of aggregate Q2 earnings growth estimates for the index since the start of 2022.

Image Source: Zacks Investment Research

What this chart is showing is that expected Q2 earnings growth in the aggregate has declined from +2.8% on March 30th to +1.9% today.

That said, there are plenty of cross currents at the sector level, with positive revisions to the Energy sector offsetting declines in most other sectors.

The second quarter 2022 earnings estimates for the Zacks Energy sector have increased +47.9% since the start of April.

Energy is not the only sector that has enjoyed positive Q2 estimate revisions; there are 5 other sectors whose estimates have gone up in varying magnitudes.

Since the start of Q2 on April 1st, earnings estimates have gone up for the Transportation, Basic Materials, Autos, Construction, and Consumer Staples sectors. Of these 5 sectors, the upgrade to the Q2 earnings outlook is particularly significant for the Transportation and Basic Materials sectors.

If we look at the aggregate Q2 revisions, after excluding the Energy sector from the mix, then the picture changes, as you can see below.

Image Source: Zacks Investment Research

Pretty much the same trend is at play with revisions on an annual basis, with aggregate estimates stable or even modestly up since the start of the year, but starting to come down on an ex-Energy basis.

I will not share those charts here to keep the length of this piece manageable, but I think it will be useful for you to see what has happened to full-year 2022 earnings estimates for the Energy sector since the start of the year.

Image Source: Zacks Investment Research

Any way you look at it, the Energy sector is in a good place at present, with a very strong earnings outlook. The relatively long-term view of the sector’s earnings picture is highlighted below.

Image Source: Zacks Investment Research

This Week’s Earnings Results

We have three S&P 500 members on deck to report quarterly results this week. These are Kroger KR, Oracle ORCL and Adobe ADBE. Of these three, Oracle and Adobe will be reporting results for their respective fiscal quarters ending in May, while Kroger will be reporting its April-quarter results.

The convention that we and other data vendors use would put this week’s Kroger results as part of the 2022 Q1 tally, while the Adobe and Oracle results will become part of the 2022 Q2 tally.

Please note that Adobe and Oracle aren’t the first S&P 500 members to report Q2 results, as two index members – Costco COST and AutoZone AZO – have already come out with fiscal May-quarter results that we categorize as part of our 2022 Q2 tally.

The Q2 reporting cycle will really get going in mid-July when the big banks come out with quarterly results. But we will have counted such Q2 results from almost two dozen index members by then.

The Current Earnings Backdrop

The chart below shows current expectations (and actuals) on a quarterly basis.

Image Source: Zacks Investment Research

For a detailed look at the overall earnings picture, including expectations for the coming periods, please check out our weekly Earnings Trends report >>>>Breaking Down the Tech Sector’s Earnings Outlook

Just Released: Zacks Top 10 Stocks for 2022

In addition to the investment ideas discussed above, would you like to know about our 10 top picks for the entirety of 2022?

From inception in 2012 through 2021, the Zacks Top 10 Stocks portfolios gained an impressive +1,001.2% versus the S&P 500’s +348.7%. Now our Director of Research has combed through 4,000 companies covered by the Zacks Rank and has handpicked the best 10 tickers to buy and hold. Don’t miss your chance to get in…because the sooner you do, the more upside you stand to grab.

See Stocks Now >>

Click to get this free report

The Kroger Co. (KR): Free Stock Analysis Report

Oracle Corporation (ORCL): Free Stock Analysis Report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

Adobe Inc. (ADBE): Free Stock Analysis Report

AutoZone, Inc. (AZO): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.